Please login to leave a comment

IN THE JOURNAL | GLOBAL PERSPECTIVES

The hidden costs of broken supply chains

With tariffs so low, what's holding up cross-border trade?

October-December 2013

By:

Jean-Pierre Fellenbok , Mark Gottfredson

For decades, governments and companies around the world have focused almost exclusively on tariffs as the biggest impediment to global trade. Despite tariffs dropping to a 30-year low, reform efforts have stalled in recent years and international trade remains seriously constrained. A big reason: the inefficiencies and chokepoints that hobble global supply chains turn out to be a much bigger factor than government-imposed tariffs in restricting the flow of goods and services across borders.

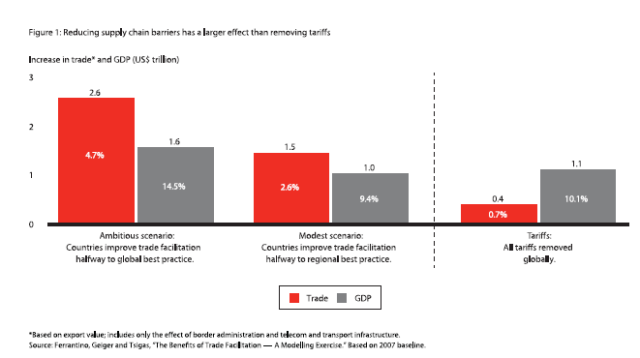

Together with the World Bank, Bain & Company has analyzed the business implications of supply chain barriers everything from border delays and inconsistent product regulations to poor infrastructure and rampant corruption — presenting our findings in a report for the World Economic Forum. Our analysis demonstrates that reducing even a subset of these obstructions could increase global GDP over six times more than removing all tariffs (see Figure 1).

That has broad, long-term implications for policymakers, suggesting that governments need to refocus their efforts on creating efficiencies in the supply chain if they want to truly unlock the economic potential of global trade. For companies looking to take advantage of international markets, the message is more immediate: making the right choices about where and how to deploy assets globally requires a full understanding and analysis of how these supply chain barriers affect return on investment. Failing to anticipate the costs and risks involved can wipe out the business advantages of sourcing, operating or selling in foreign markets.

These messages are particularly relevant for Indonesia. While the Indonesian economy has been remarkably successful during the past few years, powered by a large and growing consumer class and sound macroeconomic policies, policymakers need to pay serious attention to the performance of its supply chain. The physical characteristics of the archipelago and the growth of its economy, widely distributed over a vast territory, requires sound infrastructure such as port capacity and roads, as well as efficient systems. Indonesia still has a long way to go.

Strengthening supply links

Supply chain barriers include anything that obstructs the easy movement of goods from one link in the supply chain to the next: subpar roads, outmoded border policies, restrictive local content rules. Their effects vary by region, industry and country, but the report found that they often work in concert to slow down trade and drive up costs in both developing and developed nations. That drains resources that might otherwise be used to create jobs and increase prosperity.

Many corporate leaders know of these chokepoints from direct experience. One diversified chemical company that exports acetyl and other products to the United States, for instance, needs approvals for every shipment from as many as five different US regulatory agencies, delaying 30 percent of inbound shipments and causing cancellations from customers fed up with waiting. A global food products company sources a significant amount of its raw materials from Brazil. But a combination of poor roads and shoddy communications infrastructure slows shipments and makes them difficult to track, increasing security risks. At port, cargo “dwell” time averages five to 10 times longer than in Chile and developed nations. That drives up operating costs and forces the company to stockpile inventories, tying up working capital.

Supply chain barriers fall into four main categories: market access, telecommunications and transportation infrastructure, border administration and business environment. We identified global best practices for each category based on case studies, calculated what a country’s deviations from those standards cost it in terms of lost trade and lower GDP, and compared that to the effect of eliminating all tariffs.

The results were startling. Data showed that if countries could reduce just two of the supply chain barriers border administration and telecommunications/transportation infrastructure — halfway to their global best practice levels, global GDP could rise by nearly 5 percent, or $2.6 trillion, while trade could improve almost 15 percent. By comparison, eliminating all import tariffs could increase global GDP just 0.7 percent, while boosting trade by 10 percent. Even if countries were able to reduce barriers halfway to less aggressive regional best practice levels, global GDP could rise by 2.6 percent still outpacing the benefit from tariff elimination.

The efforts to eliminate tariffs remain an important area of focus for governments. But a coordinated push to free up supply chain chokepoints will give policymakers significantly more leverage to increase economic growth through free trade. Why? While both supply chain barriers and tariffs increase the cost of trade, barriers create greater inefficiencies than tariffs because they often represent a pure waste of resources rather than a simple transfer of payments to the government. Developing nations, in particular, stand to benefit from improvements. So too would small and midsize companies, many of which are blocked from selling internationally by prohibitive supply chain barriers that strain their limited resources.

Getting past the tipping points

While tariffs can generally be eliminated with the stroke of a pen once political obstacles are addressed, eliminating supply chain barriers is a complex task that requires coordinated policy action and investment. As with tariffs, regulators have to deal with reluctance from companies and local industries protected by supply chain barriers. And they have to make smart choices about which changes will have the greatest impact.

Real improvement depends on achieving specific “tipping points” of new efficiencies across various kinds of barriers that encourage companies wary of wasting resources to risk new investments in a given market. For example, if the market’s supply chain barriers add 10 percent to a company’s cost of doing business, reducing those barriers to just 2 percent won’t likely spur new investment activity. But the research clearly shows that once those tipping points are reached, the impact on trade and foreign investment can be dramatic, as companies move to take advantage of newly opened markets and pathways to increased growth.

Consider the results of a pilot program initiated by eBay, the global online commerce platform. In many ways, the Internet has created vast new low-cost opportunities for eBay sellers to connect with previously inaccessible customers around the world. But when eBay surveyed its merchants — most of them small businesses — it found that the opportunity to sell internationally was too often going unrealized. Efforts to develop all but the most accessible foreign markets are still inhibited by complex regulations, poor international shipping services and high fixed costs, meaning merchants with narrow resources could risk doing business in only a limited number of foreign markets.

Responding to the problem, eBay set up a pilot program to help eliminate the barriers. For a preselected group of merchants, it made listings available to a global customer base and then undertook steps to ease reluctance among both buyers and sellers by providing full transparency on what it would cost to ship goods and when they would arrive. It worked through shipping issues and facilitated communication among people who spoke different languages. Preliminary results indicate that making these improvements could lead to a 60 percent to 80 percent increase in cross-border activity among these Internet-enabled small businesses. Given the global importance of small companies in terms of job creation and economic activity, the broad benefits of such an increase in trade activity would be substantial.

What companies can do right now

While governments can help reduce supply chain barriers, companies can’t afford to wait. As a business matter, they must make investments in their global operations right now to remain competitive. Recognizing the importance of “hidden” supply chain costs, leading companies are incorporating more rigorous due diligence into their decisions about where to produce and sell their wares. For executive teams, the report’s findings offer important insights on key areas to consider when analyzing the true costs of doing business in a particular country or region.

Even large companies often fail to anticipate the costs and risks imposed by supply chain barriers. No central data bank exists that can tell an executive team how long its products are likely to be delayed at a given border or what the average speed of trucks is along a specific shipping route or transportation corridor. Yet leaving barrier-related costs out of the equation could open companies to hidden costs that significantly erode returns.

One apparel company established operations in Madagascar, for instance, only to find that supply chain barriers seriously limited its opportunity there. The company was initially attracted by the country’s low labor costs and proximity to high-quality African cotton suppliers. But its products are frequently delayed at the border and moving finished goods the 330 miles from mill to port takes 14 hours — not bad compared with many African countries but far longer than comparable supply routes in Asia. These supply chain costs completely offset Madagascar’s labor-cost advantage and undermine the company’s ability to compete in segments of the “fast fashion” business, where speed to market is crucial. Producing some apparel in Madagascar makes sense because the company can ship tariff-free to Europe and compete with Asian producers that still face duties — a reminder that tariffs do still matter. But if those tariffs disappeared, Madagascar would not be competitive.

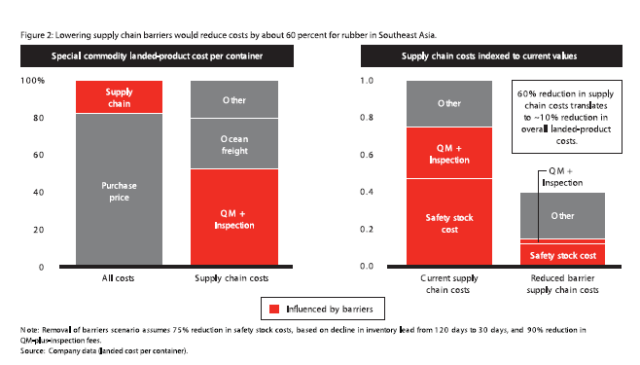

The message is that supply chain barriers can significantly upset conventional cost and revenue calculations. For instance, Bain estimates that addressing supply chain barriers would reduce supply chain costs by 60 percent for rubber in Southeast Asia and result in 10 percent lower total landed costs (see Figure 2).

Most companies involved in cross-border trade have become experts in standard return- on-investment analysis to justify investments abroad. They know how to evaluate tax breaks, labor costs, capital expenses and the costs associated with logistics, sourcing equipment and finding raw materials. But often these traditional analyses fall short when it comes to capturing the true cost of doing business.

Breaking down the costs

Over the years, Bain has worked with many companies that were weighing the merits of trading with Mexico or moving production there, especially after the North American Free Trade Agreement ended most formal trade barriers on the continent. While a traditional analysis might show that Mexico has a 25 percent cost advantage relative to the US and Canada, more than half of that advantage could be eliminated by supply chain friction costs. In doing the analysis, we’ve been able to quantify those costs and how they affect a company’s real return on investment.

The benefits of investing in Mexico are well known. A hypothetical manufacturer weighing whether to relocate production capacity there would see that hourly wage rates are about one-fifth of what they are in the US, while capital expenditures related to building facilities are typically 10 percent lower than in the US or Canada. Depending on the company’s product mix, there can be other advantages as well. Products best suited for production in Mexico are those with the highest level of direct and indirect labor content. They are made from basic materials that can be easily sourced in Mexico. And because those materials have to travel long distances to market, they are typically nonperishable (to avoid the cost of refrigerated trucks) and have a high value-to-weight ratio.

Even if those considerations support a positive investment conclusion, however, a number of hidden costs complicate a more thorough analysis. Mexico’s lack of federal and provincial tax breaks, for instance, can add 1 percent to investment costs up front. The lower productivity of Mexican hourly workers, coupled with a lack of automation, means a company might have to boost staffing levels 25 percent, erasing some of the labor-cost advantage.

Transporting goods in Mexico is also a problem. Gaps in road and rail connections require shipments to travel extra distances that will eat into margins. And while Mexican trucks entering the US no longer have to switch drivers and cabs, as they did until 2011, they do have to buy US insurance at the highest possible rate. Then there’s safety. High crime rates in Mexico might require the investing company to take extraordinary measures to safeguard building assets as well as goods in transit putting armed guards on all trucks, for instance. Security measures alone can boost fixed costs by as much as 7 percent per year.

Clearly, many companies have profitable operations in Mexico and it might make sense for our hypothetical manufacturer to establish a beachhead there as well. But the key to any such decision is to take a full accounting of all the relevant cost inputs, while extrapolating the consequences of supply chain inefficiencies: will delays force a company to stockpile buffer inventories, which tie up working capital and add to direct costs such as warehousing? If so, what risks follow in the form of depreciation, spoilage or production bottlenecks?

When these costs are factored in, returnon- investment cost calculations will be adjusted upward to reflect the level of risk anticipated. But companies often fail to take these costs into account; as a result they find themselves locked into uneconomical production and marketing decisions.

A domestic agenda for Indonesia’s supply chain

The advantages of Indonesia as a market to invest in, such as relatively low wage rates, access to the largest consumer market in Asia outside of China and India and a large and growing middle class, are obvious. However, as is the case with Madagascar and Mexico, Indonesia also faces serious supply chain costs, more so now than before.

In 2007, the World Bank’s Logistic Performance Index (LPI) ranked Indonesia 43rd. However, in 2010, the same index placed Indonesia 75th out of 155 countries. Although Indonesia’s many improvement initiatives moved it to 59th place in 2012, its LPI score is still lower than many of its neighbors such as Malaysia, Vietnam, the Philippines, Thailand and India.

At Jakarta’s Tanjung Priok port, dwelling time recently reached a worrying level of 8.7 days, compared to five days in Thailand, and 1.2 days in Singapore. This is due to a combination of factors that compound each other: border administration issues, business practices and poor road infrastructure. As the chief executive officer of the state-owned Indonesian Port Corporation observed, the amount of goods entering the Customs and Excise Office “red line” has reached 25 percent, which is five times higher than the average of any port in the world. The fact that there are more than 4,000 containers “stored” at the port also negatively affects the loading and unloading process. Finally, due to inadequate road infrastructure, it takes a full day to transfer these containers to a storage location nearby in North Jakarta.

The issues highlighted above are neither new nor limited to Tanjung Priok. According to a World Bank survey, while most firms are satisfied with the factory gate price and quality of Indonesian products, they find that the main constraints for business transactions are the high transportation costs and unreliability of delivery schedules.

Research by The Asia Foundation and University of Indonesia in 2008 found that the operational cost of trucks in Indonesia was 34 cents per kilometer, while the average cost for all of Asia was significantly lower at 22 cents. Road and rail infrastructure in Indonesia is lagging behind many of its neighbors. In 2010, Indonesia’s road density (kilometers of road per 100 inhabitants) stood at 20, while China’s was 29 and Malaysia’s was 50. Indonesia’s traffic conditions might worsen should this issue not be addressed adequately, considering that its road growth is 1 percent per year while the number of vehicles on the road grows at 9 percent per year. In terms of rail transportation, Indonesia has half the number of railway lines per inhabitant as China, Malaysia and Thailand.

Such impediments introduce more time and costs to the supply chain. They also make it less reliable. According to the World Bank, logistics operators in Indonesia report that almost one-third of all shipments are not delivered as scheduled. As a consequence of this uncertainty, manufacturers are forced to maintain higher inventory levels.

The Indonesian government is well aware of this and has taken measures to remedy the situation. It includes short-term solutions including extending the customs and excise office opening hours and removing containers from the port to address the situation at Tanjung Priok. It also includes longerterm solutions such as establishing the New Tanjung Priok port, improving road infrastructure and developing a logistics blueprint in 2008 as part of the new National Single Window System.

However, given the impact of supply chain performance on the country’s competitiveness, Indonesia’s policymakers and businesses need to look at supply chain costs and inefficiencies holistically, focusing on areas of improvement with the highest return on investment for the economy, setting goals that are ambitious enough to “pass the tipping point,” and making a difference in business behavior and putting in place the metrics that allow progress tracking.

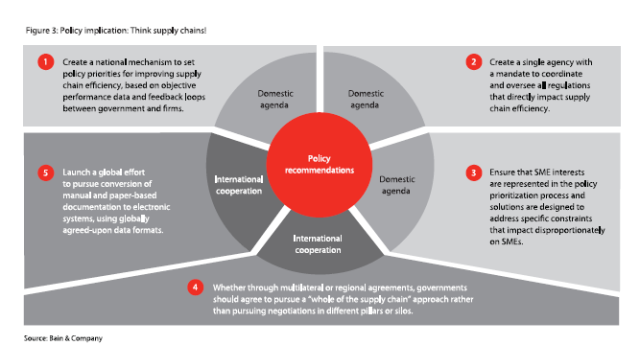

From a national policy standpoint, Indonesia should create a domestic agenda to improve supply chain performance, which could involve (see Figure 3):

• Creating a national mechanism to set policy priorities for improving supply chain efficiency, based on objective performance data and feedback loops between government and firms.

• Creating a focal point within government with a mandate to coordinate and oversee all regulations that directly affect supply chain efficiency.

• Ensuring that the interests of small and medium-enterprises are represented in the policy prioritization process, and that solutions are designed to address specific constraints which disproportionately impact them.

Looking for ‘hidden’ costs

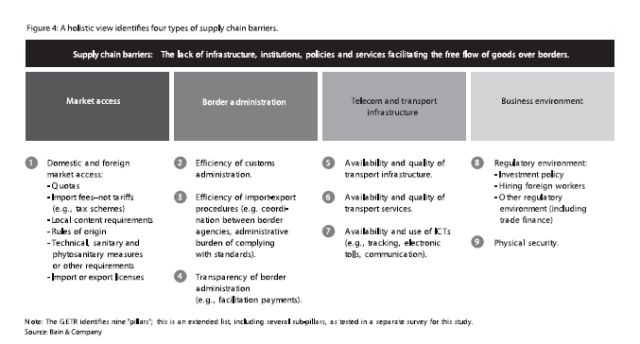

Clearly, supply chain barriers to trade are both complex and widespread. A more comprehensive approach to foreign investment decisions means recognizing costs in four important categories of the supply chain (see Figure 4). Executive teams can begin by asking some key questions relating to each category:

Market access

• Do you know how many regulatory agencies you have to deal with as you move goods into or out of your chosen market?

• Do you have a list of the licensing regulations that apply to your product or service?

• Are there preferential rules or regulations that give local companies a leg up in the market? Will that affect your costs or competitiveness?

Border administration

• What percentage of shipments will be inspected at the border, on average? How does that compare with other markets?

• What is the typical delay time at a particular border or port, and what will that cost in terms of spoilage, theft or the need to stockpile additional inventories?

• How often do border officials demand “facilitation payments” to move goods efficiently? Are you prepared for the repercussions of not paying (i.e., potentially severe delays)?

Telecom and transportation infrastructure:

• Does the country have an electronic system at the border, allowing shippers to declare goods in advance and speed up processing? Are those systems reliable and used consistently?

• How fast, on average, are truck or rail shipments able to move to and from key ports? What are the common delays and how costly are they?

• What special fees, licenses or other special regulations do local authorities impose on truckers that add costs or slow the movement of goods?

Business environment

• What are the political and administrative realities in your chosen market, and how will that affect the ease and security of doing business there?

• Do businesses enjoy the support and encouragement of government officials, or is there a history of random taxation, excessive fees or other attempts to extract value from the private sector?

• Are the rules and regulations that pertain to your business clear and consistent? Are there established procedures for working through them?

All of these costs can be estimated to gauge the effect on potential investment returns. But if your team can’t provide definitive answers to questions like these, moving forward can have real repercussions. In Brazil, for instance, an attempt to build an electronic freight invoicing system should have helped speed shipments. Instead, subpar government information and communications technology systems couldn’t handle the volume and often crashed, causing longer delays than the old system.

Border regulations that affect efficiency also vary widely: an express delivery company estimates that inspection rates on its shipments range from 2 percent in the Netherlands to roughly 10 percent in Mexico. A pharmaceutical company that has won “trusted trader” status in both China and Canada finds that Canada’s streamlined system gets goods on their way quickly while China’s cumbersome procedures cost the company six times as much due to delays and related expenses.

When it comes to business environment, developing countries can often promise as many barriers as opportunities. As the consumer goods company doing business in Africa has found, security concerns and efforts to cope with a highly disruptive sociopolitical environment often create a cascade of costs that can upset even the most carefully considered investments. Conditions are more stable in China, but one large semiconductor manufacturer reports that it constantly wrestles with various rules that are vague and inconsistent. Struggling to comply with them can often lead to confusion and delays.

For every company and industry, the supply chain challenge is different. But all share the need to recognize potential barriers where they are most likely to be encountered and to develop a full understanding of how they will impact business. A reliable assessment of what it truly costs to operate in a given market is the necessary foundation for the next step in evaluating foreign investment: comparing alternatives and deciding which best suit a company’s long-term strategy and business objectives.

Global trade has increased sharply during the past 30 years, and the opening of markets long considered inaccessible has created rich opportunities for companies of all sizes in every industry. But the companies that get it right are the ones that can best identify and analyze the real cost of capturing those opportunities and avoid the mistake of going in unprepared.

Calculating the biggest barriers

Economists and executives have known for a long time that supply chain barriers are real. But the full scope of their corrosive effect on global trade and prosperity emerges when a quantitative model is combined with on-the-ground case studies showing how companies actually think about their supply chains and how that affects their decision-making.

Many studies have measured the macroeconomic effect of supply chain barriers. But most lack insight into how those issues affect corporate investment and strategy. By augmenting their analysis with 18 detailed “real-world” case studies, Bain & Company, along with economists from the World Bank, the World Economic Forum and the US International Trade Commission, were able to gain those insights, leading to a set of policy recommendations aimed at breaking down impediments to action.

The study identified four broad categories of supply chain barriers: market access, border administration, transportation and telecommunications infrastructure and business environment. Researchers focused on the two that have the most immediate upside: border and infrastructure-related barriers, building models to measure the impact of these barriers on GDP by region and comparing the results to the effects of eliminating tariffs. They used the case studies representing major industries, barriers and supply chain steps to illuminate real problems and estimate how improvements in these categories would affect behavior.

The study shows plainly that policies to improve border administration and infrastructure could have six times the impact on global GDP as the elimination of all tariffs, largely because improvements would eliminate so much of the waste and inefficiency that hobbles growth. But the data also suggests that improvements could be even more dramatic. If policymakers could forge improvements across all four of the barrier categories, the positive effect on GDP would be approximately 70 percent higher. This is clearly something worth striving for.

Mark Gottfredson is a partner with Bain & Company, based in Dallas, Texas, and a senior member of Bain’s Performance Improvement practice.

Jean-Pierre Fellenbok is managing partner of Bain Indonesia, based in Jakarta.

COMMENTS

STRATEGIC REVIEW EVENTS

MOST READ ARTICLES

resized.png)

STAY CONNECTED TO SR INDONESIA